In considering this I want to break those needs into four categories:

- Needs the client has identified and is having met by you

(Example – annual accounts and tax returns) - Needs the client has identified and is having met by another provider

(Example – bookkeeping or financial planning) - Needs the client has identified which are not being met by anyone

(Example – to understand fully their own numbers) - Needs the client is not aware of but which you could see and meet

(Example – tax or estate planning)

Clearly there is opportunity in 2, 3 and 4 and for me the most obvious way to be able to realise the opportunity is through conversations with your client.

Client conversations

It has consistently been my experience over 30 years (both in serving clients from within an accounting firm and as a coach, consultant and mentor speaking to owners and managers almost every day) that it is easy to get caught up in the day to day of “getting the work done” without realising that an important part of that is the conversations you have with your clients about themselves and their businesses.

If you have these conversations with your client you are almost certainly going to get a better understanding of their needs and be better placed to meet them. If you uncover needs that are being met by another provider then be sure not to “bad mouth” the provider but rather acknowledge that you would also be able to assist in the area. It would be good to probe a little to understand why you were not considered and it may be as simple as “I did not know you did that”. Ouch!

Your client conversation may also identify a need that the client has already identified but for whatever reason has not got around to talking to you or any other provider about. Your client conversation could very well also lead to the client becoming aware of one or more needs that were not aware of. In both cases you are well placed to demonstrate how you can meet that need.

Share of wallet

Categories 1 and 2 above together allow you to calculate your “share of wallet” with a client. In essence your share of wallet is the percentage of $ spent with you against the total $ spent on all the services you could provide. What services do your clients buy from you? Are they buying all of the services they could be? Or are they buying some services from someone else that you (could and should) provide? Have you ever thought about this?

In the big end of town the share of wallet is often managed by having panels of service providers, particularly for lawyers. The business may have very clear process for it divides the share of wallet for each panel member based on certain criteria. Most SME’s will not formally do this but perhaps they do shop around or worse still just don’t understand the full range of services you can provide them and go somewhere else assuming you can’t help.

My own business is a good example. In working with accounting firms I provide coaching, consulting, training, mentoring and facilitation services across pretty much all aspects of the firm. (You can see them here if you are curious) I want to make sure that for my existing clients they have no need to go to other providers if, and this is key, I genuinely believe I am the best person to deliver those services.

I certainly don’t want a client to say “We got X to facilitate our planning days because you don’t do that” Oops, oops and oops! I say to the client “I love doing planning day facilitation and have done quite a few” So why didn’t the client ask? Is the relationship not such that they feel comfortable to check? And why had I not made that client aware of my full capability? (This has not happened to me, but it makes the point I hope!)

It is an important concept because of the conventional wisdom that it is easier to sell to existing clients than win new ones.

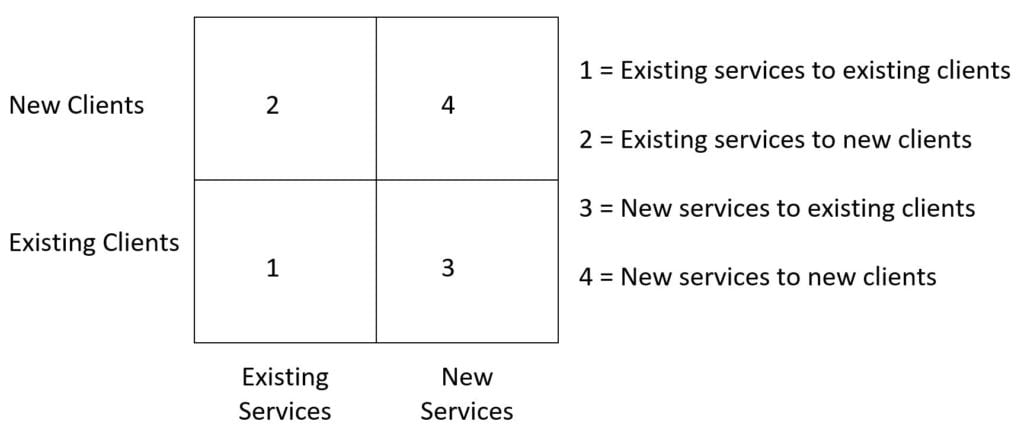

Consider the simple matrix below.

Client / Service Matrix

Clearly 1 should take the least effort. You already have a relationship with these clients and you are already providing these services to other clients.

2 and 3 may take different amounts of effort depending on the circumstances of your firm. If you have strong capability and capacity to win new clients but are weaker when it comes to developing new services, then 2 will be easier than 3. For some firms it will be the other way around.

What is clear, is that 4 is the one that is going to take the most effort.

The biggest opportunity in most firms – the low hanging fruit

Go for the low hanging fruit – 1 is the place to be! At least to start with. In my experience most firm owners and managers say there is a pile of work they could be doing for existing clients if only they could get to it. Step back and ask yourself if you need to build some additional capacity to be able to do this work.

There is another reason why making sure you have 1 covered is important. If another service provider “gets their foot in the door” they may try to takeover other services you are providing. Don’t let that happen! Get on the front foot with your clients.

So how do you do that?

I think there are two pretty straightforward things to start with:

- Track what services you provide to which clients

- Have a structured approach to educating your clients on your capabilities

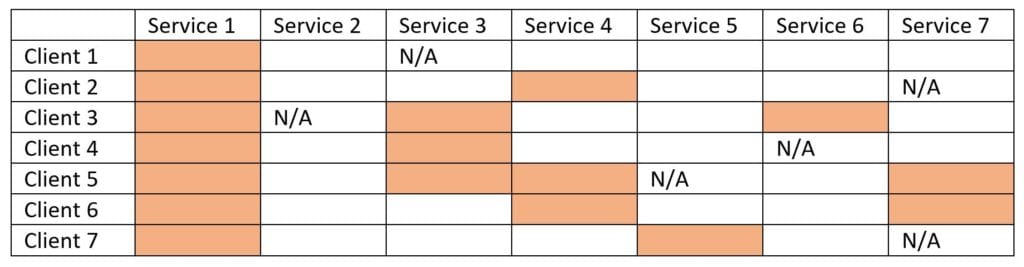

To track services you could do a matrix that has clients listed down the page and services list across the page, like the example below.

Clients and Services Matrix

Depending on what reporting you have set up for your practice management system this should be able to be extracted relatively easily and show the fee for each service type delivered.

In this matrix the shading indicates that service is being provided to the client, N/A indicates that it genuinely not a service applicable to that client and the blanks indicate the huge opportunity available to you.

Are you taking advantage of this opportunity?

If not what can you do to change that?